#BlueRevolution - Time to take the plunge

The Fish & Seafood sector provides a historically favorable opportunity. Valuations are at the same level as 2013/2014, while companies have been able to strengthen their positions.

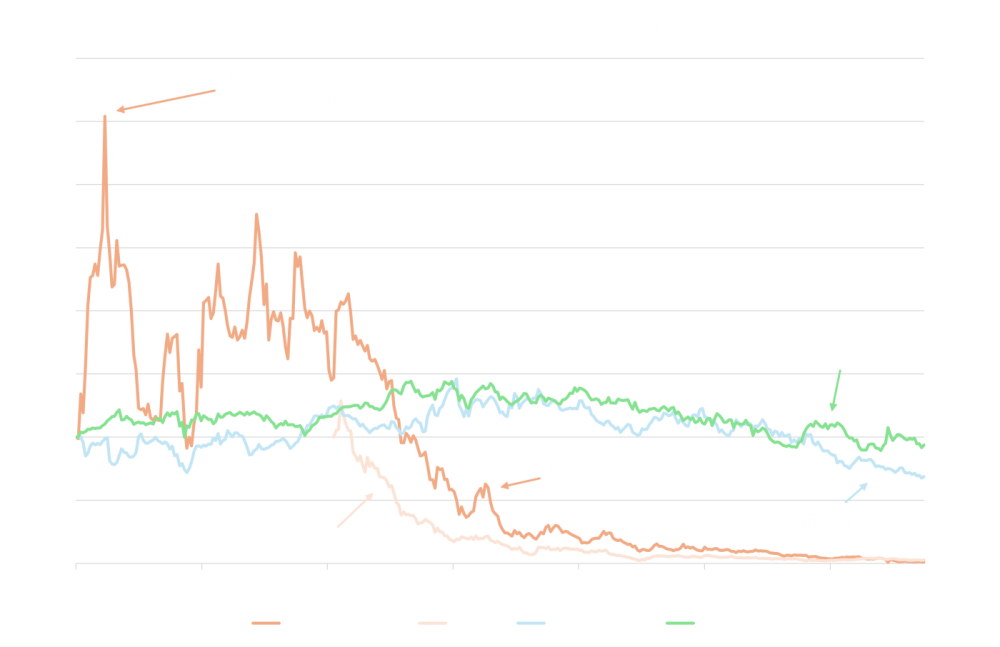

It began like a quiet revolution on the plate – and, as so often, ended on the stock market with a painful landing. Between California and Copenhagen, a new generation of food companies emerged, promising nothing less than the reinvention of our global food system. Investors leaned in decisively. Plant-based burgers became symbols of a supposedly better future – and stock market favorites.

Just a few years later, however, the euphoria feels like a relic of a different market phase. What was marketed as a megatrend turned out, for many investors, to be a lesson in inflated expectations, fragile business models, and the old market truth that compelling narratives rarely equate to strong returns.

While valuations collapsed, a quieter yet potentially more durable shift has been unfolding in the background: policymakers, consumers, and capital markets are rediscovering what had long fallen out of focus – real, nutrient-dense foods. This marks the beginning of a second phase in the food trend, one driven less by vision and more by fundamentals.

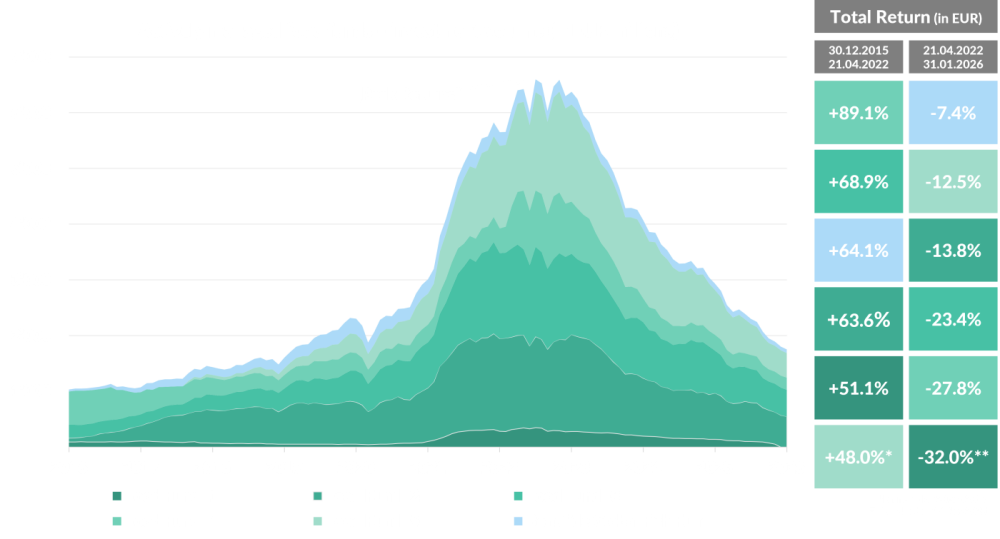

Not only individual stocks benefited from the food hype. Thematic investment funds focused on food, agribusiness, or “smart food” recorded substantial capital inflows, particularly between 2020 and spring 2022.

Many of these funds delivered cumulative returns ranging from approximately 50% to nearly 90% at the peak of the bull market (January 2016 to April 2022). At times, they performed on par with global equity indices – yet were supported by a far stronger narrative centered on future food, sustainable nutrition, and new protein sources.

Assets under management in these strategies reached a peak in 2022. Since then, a clear decline in aggregated fund assets has emerged. Rising interest rates, declining volumes in branded products, and setbacks at companies like Oatly & Co. triggered billions in outflows.

The pattern is reminiscent of previous market cycles. A historical comparison can be drawn with commodity funds following the so-called “commodity supercycle” up to 2011: years of rising inflows, a clearly defined “peak return,” followed by a prolonged consolidation phase.

| Company | Equity Story | Performance |

| Beyond Meat | Symbol of the meat substitute boom, IPO 2019 | Share price decline from USD 239 to USD 1 | −99% |

| Oatly | IPO 2021 as global oat milk champion | −95% since IPO |

| Nestlé | Diversified food conglomerate | −40% from peak in early 2022 (in Swiss francs) |

| Kraft Heinz | Buffett-backed investment | −50% since 2019 |

| Company | Beyond Meat |

| Equity Story | Symbol of the meat substitute boom, IPO 2019 |

| Performance | Share price decline from USD 239 to USD 1 | −99% |

| Company | Oatly |

| Equity Story | IPO 2021 as global oat milk champion |

| Performance | −95% since IPO |

| Company | Nestlé |

| Equity Story | Diversified food conglomerate |

| Performance | −40% from peak in early 2022 (in Swiss francs) |

| Company | Kraft Heinz |

| Equity Story | Buffett-backed investment |

| Performance | −50% since 2019 |

The causes are multifaceted. Beyond Meat continues to struggle with losses and declining revenues. Oatly faces increasing competition from private labels and remains unprofitable. At the same time, even established food giants such as Nestlé and Kraft Heinz are confronted with rising costs and increasing pricing pressure from retailers.

This development mirrors other industry cycles: in sectors such as smartphones or solar energy, early pioneers rarely generated the best long-term returns. Profitability often materialized later among companies with scale advantages, stable supply chains, and strong brands.

Several structural factors explain the weak performance of many food stocks in recent years:

1. Shift in the interest rate regime

With the sharp rise in real interest rates since 2022, growth stories with profits “far in the future” have lost significant appeal. Companies without established profitability models were particularly affected.

2. Rising production costs

Raw material, energy, and logistics costs increased globally. At the same time, consumers responded to higher food prices by shifting toward more affordable private-label products.

3. Low barriers to entry

Although studies continue to project growth in plant-based proteins – in some cases reaching market shares of 11% to 22% by 2035 – numerous competitors quickly entered the market.

In parallel with capital market developments, the political and societal debate around nutrition is also evolving.

The first U.S. food pyramid from 1992 placed grain products such as bread, rice, and pasta – with six to eleven servings per day – at the base of the diet. Proteins and fats, by contrast, were to be consumed sparingly.

With the new dietary guidelines for 2025 to 2030, a clear shift is emerging. Protein-rich foods, including fish, eggs, and dairy products, are gaining prominence. At the same time, the guidelines increasingly emphasize unprocessed foods and whole grains.

In practical terms, this means: the focus is shifting from highly processed products to natural foods with higher nutritional value.

For certain segments of the food industry, this shift could create structural opportunities – particularly for producers of high-quality proteins.

The story of the food hype in equity markets once again illustrates a familiar pattern: new trends are often initially overvalued before sustainable business models emerge over time.

While many early stock market favorites in the plant-based segment have lost substantial value, one core trend remains intact: global demand for high-quality protein sources continues to rise.

With a growing global population, rising incomes, and an increasing focus on health and nutrition, the efficient production of protein is becoming strategically more important. In this context, segments such as aquaculture and fisheries are attracting renewed attention from institutional investors – not least due to stable demand, robust cash flows, and attractive valuations. The strategy of the Bonafide Global Fish Fund reflects this development, with a portfolio currently offering approximately 4.5% dividend yield and trading at a moderate valuation level of 13x P/E.

The key lesson from recent years is clear: not every food innovation translates into a successful equity story. However, where structural demand, efficient production, and stable margins converge, long-term investment opportunities emerge.

Or, to summarise it in one guiding principle:

Comments