1. Chile Report: Salmon Farming

At the beginning of 2019, we took the opportunity to visit salmon farming operations in the Chilean summer.

Whilst the Norwegian salmon industry is once again generating a ‘Wow’ effect with its biomass growth in the first half of 2026, the stock market remains disappointed. Expectations for the price of salmon have had to be revised downwards for the second year running since 2025. Yet the current situation is partly the result of past investments that deserve a ‘return’. Furthermore, the seasonality in supply seems to be disappearing, which is extremely positive for the value chain and demand in the long term. An article on the causes and effects of structural developments from a multi-year ‘bird’s-eye view’.

Farmed salmon begin their lives on land and are transferred to fjord cages when they weigh around 50 grams at the earliest, where they grow to slaughter weight in just under two years. However, regulations in open waters are strict: each farm has a maximum biomass (tonnes of live fish) that must never be exceeded. Nevertheless, in order to scale up production in the medium to long term, farmers began investing in expensive land-based facilities more than a decade ago. Depending on the region, the salmon grow to up to 1 kilogram there before being sent to the regulatory ‘bottleneck’ in the fjord. As a result, it takes them only 12 to 15 months to reach slaughter weight instead of 20, which enables a higher throughput volume. It took several years for these enormous land-based farming facilities to become operational, and the full effects have only been evident for a few quarters. Larger fish are also more robust, so the time windows during which salmon can be transfered to seawater have widened, offering potential for optimising the farming schedule.

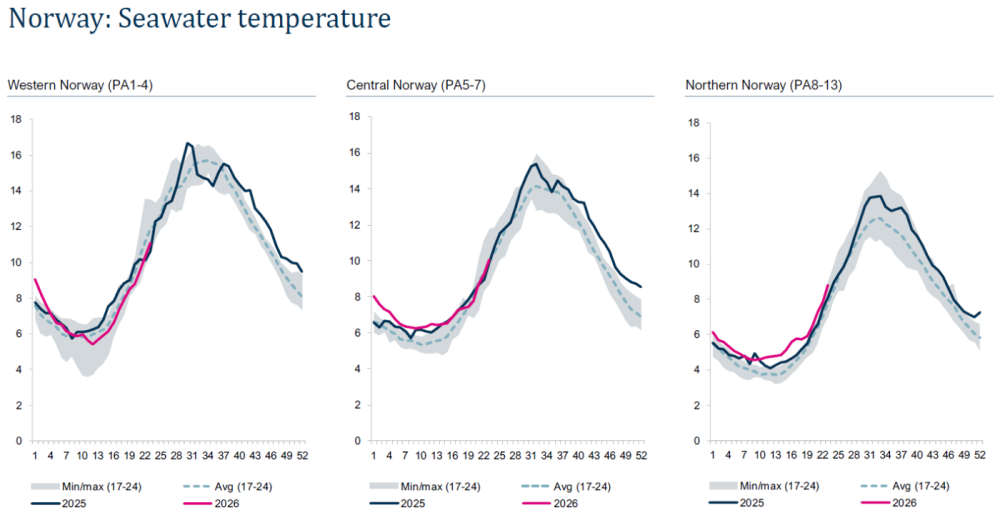

Open-water aquaculture is no different from land-based agriculture. It relies on natural capital which is volatile and unpredictable. The most significant factor is water temperature. Atlantic salmon thrive best at temperatures between 8 and 14 degrees. Temperatures below or above this range are not problematic in themselves, but they do affect the fish’s appetite and, consequently, their growth. The Norwegian coast has been experiencing slightly milder temperatures for some time now, and suddenly the fish are growing even in winter. This is generally a positive development, but it comes as a surprise to the fish farmer and disrupts their harvest planning. Added to this is the fact that investments have been made even in the fjords. For example, in submersible cages from AKVA Group, where the salmon encounter more consistent water temperatures and also grow faster.

The third key factor is the health of the salmon. Monthly mortality rates are at record lows, whilst TV documentaries on salmon farming continue to try to convince us that companies do not care about animal welfare. The lower mortality rate is, on the one hand, the result of reduced stress due to more stable water temperatures, but also of the investments mentioned above. Larger fish are more robust, and temperatures are less prone to fluctuation a few metres below sea level. Furthermore, a vaccine has been successfully developed against a specific bacterium that has been causing winter sores since 2019. The industry is also providing better protection for the salmon against sea lice by using gentler treatment methods and preventive measures.

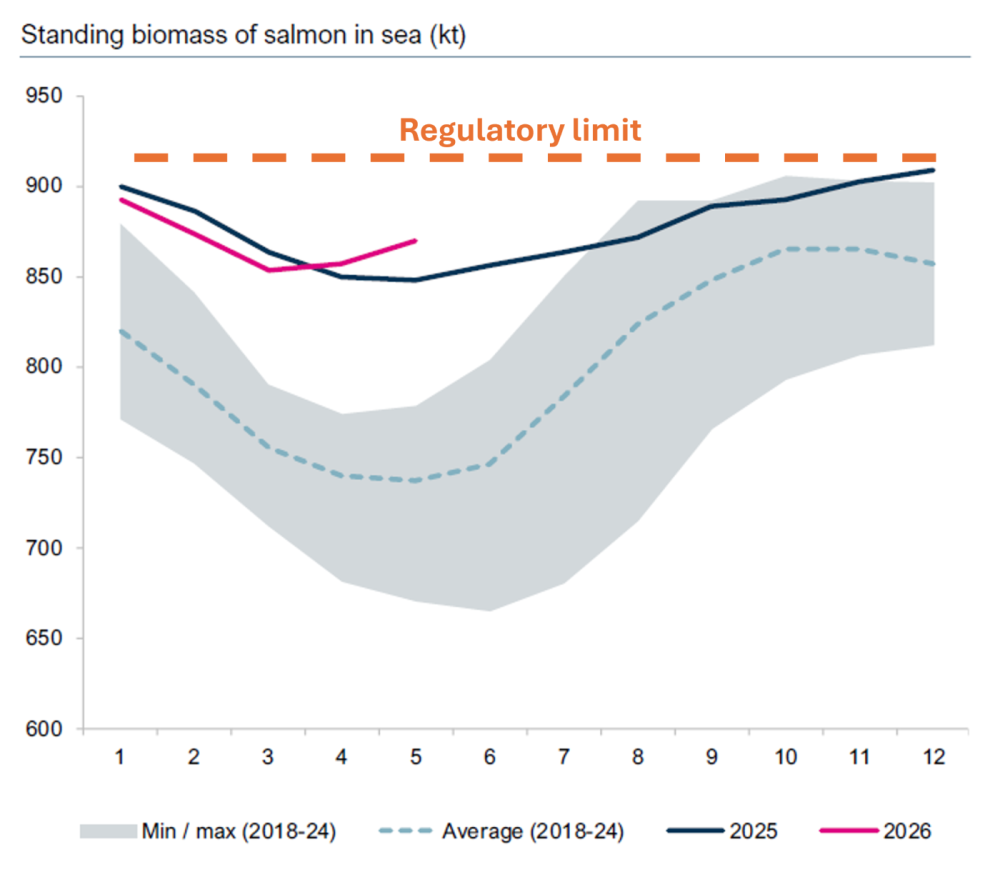

We have been witnessing for around 18 months what happens when all the factors mentioned above come into play at the same time: Norwegian biomass has remained close to the regulatory maximum limit for almost the entire year. Aggregated across all facilities in the fjords, this amounts to around 900,000 tonnes of live salmon by volume – approximately 450 million fish.

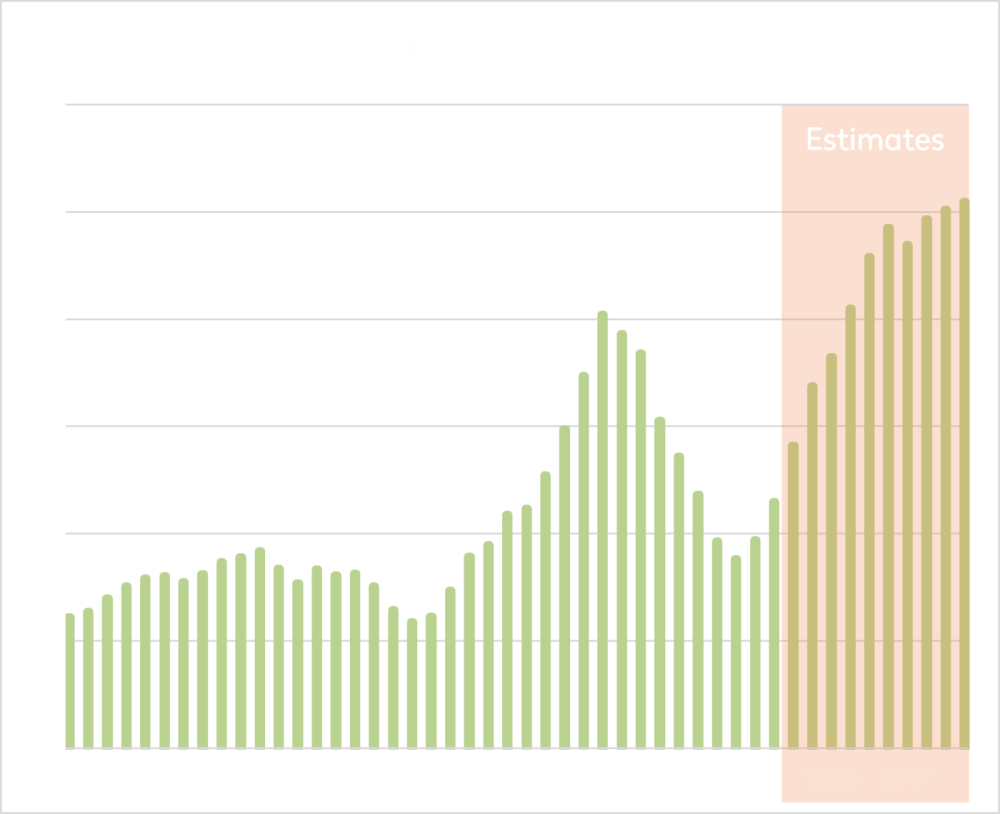

As can be seen in the graph on the left, this marks the second time since 2025 that there has been a stark deviation from the historical trend of previous years. From January to April, it was customary for biomass to shrink due to more challenging rearing conditions, with the regulatory maximum limit remaining well out of reach. The data for the last two years now seem to suggest that the industry has cracked the code, with the seasonality of the harvest visibly decreasing. Experts remain divided as to whether this is now structurally set in stone or was merely a case of ‘lucky weather’.

As soon as individual farms reach the maximum permitted biomass, they are obliged to harvest at least some of the salmon. These – previously unplanned – additional volumes must then be sold in a market that was accustomed to low volumes and high prices prevailing in the first half of the year. Buyers suddenly find themselves in a position of bargaining power, as fish is a highly perishable product and can only be stored at great expense in a cold store. Since, in an open market, the marginal quantity always determines the price, salmon prices plummeted to levels more typically seen during the peak months of August and September. In figures, Norwegian supply grew by 12% year-on-year in 2025, or 187,000 tonnes, to a total of 1,697,000 tonnes. In addition, by May 2026, there had been a further 6% year-on-year increase, amounting to 30,000 tonnes to date.

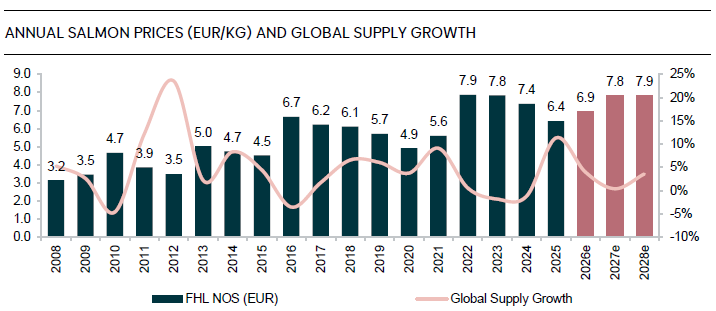

The raw materials dilemma – where excessive growth in supply drives prices down in the short term – is certainly not a new phenomenon. The current phase has also served as a test of just how strong demand for salmon actually is. And the results have been consistently positive. Although salmon is still more expensive than pork and chicken in supermarkets, sales figures in Europe and Asia are encouraging. A quarter of the additional volume in 2025 went to China alone, whose population is crying out for high-quality protein. Over several years, the trend of global demand growing by around 6–7 per cent per annum has been confirmed. Accordingly, the price of salmon in 2026 has also recovered from the lows of 2025.

What has taken a back seat is the production cost per kilogram of salmon. With double-digit growth rates, unit costs are falling significantly. For example, MOWI reported a 10 per cent reduction in costs per kilogram for the first quarter of 2026 compared with Q1/24. Furthermore, integrated salmon farmers such as MOWI and Lerøy Seafood, which operate ‘value-added’ segments, benefit from lower input costs in this area, thereby smoothing the group’s results.

As is well known, we do not have a crystal ball either. However, we observe that the stock market is currently being driven too heavily by negative media coverage. Salmon farmers are defensive growth companies that have been priced as ‘value’ stocks for some time now. The trigger for a repricing will be (at last) rising profits. And this will begin as early as 2026, albeit not to the extent that was expected at the start of the year. If market expectations are met over several quarters, confidence will return. And with confidence in sustainable, attractive profit growth comes an expansion in valuations. The stage is set for the ‘Double Whopper’ – that’s what we call profit growth paired with valuation expansion.

Comments